⚠️ Financial Disclaimer

The information provided in this article is for educational and informational purposes only and should not be construed as financial, investment, or trading advice. All data and analysis reflect opinions current as of publication and may change without notice. Always conduct your own research or consult with a licensed financial advisor before making investment decisions. Past performance is not indicative of future results.

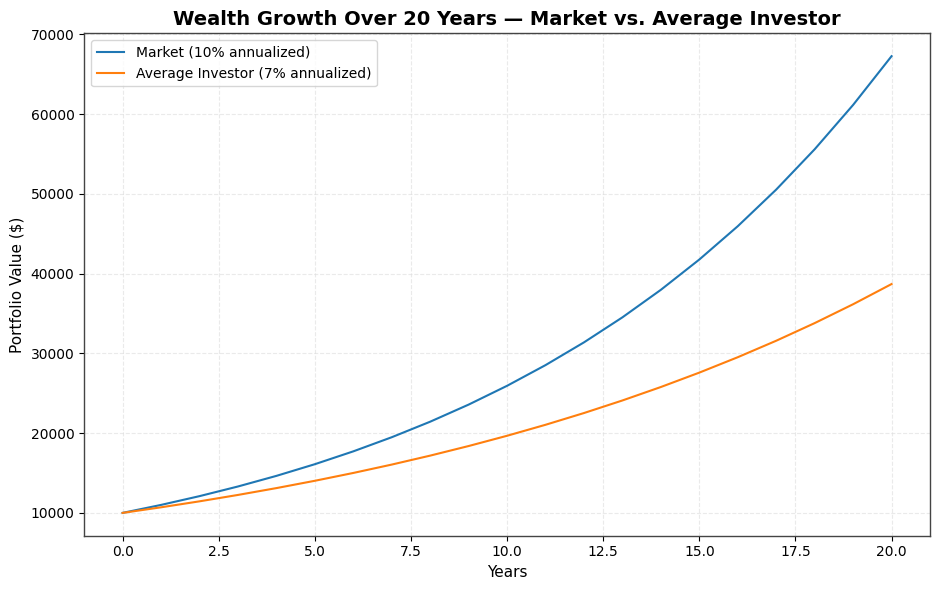

The past five years have produced one of the strongest market rallies in history. Artificial intelligence has become the driving force behind a global surge in technology valuations, lifting the S&P 500 to new records and reshaping nearly every major sector. Yet despite the broad opportunity and the accessibility of investing tools, most investors have still fallen short of the market itself.

This outcome is not new. It has repeated through the dot-com boom, the post-recession rally of the 2010s, and the recovery that followed the pandemic. Even in an era defined by innovation, zero-commission trading, and data transparency, investor returns continue to trail market performance.

According to DALBAR’s 2025 report, the S&P 500 gained roughly 25 percent in 2024, while the average equity fund investor earned only 16.5 percent. The difference was not due to fund fees or poor stock selection. It was caused by behavior — by when investors chose to buy, sell, or hold.

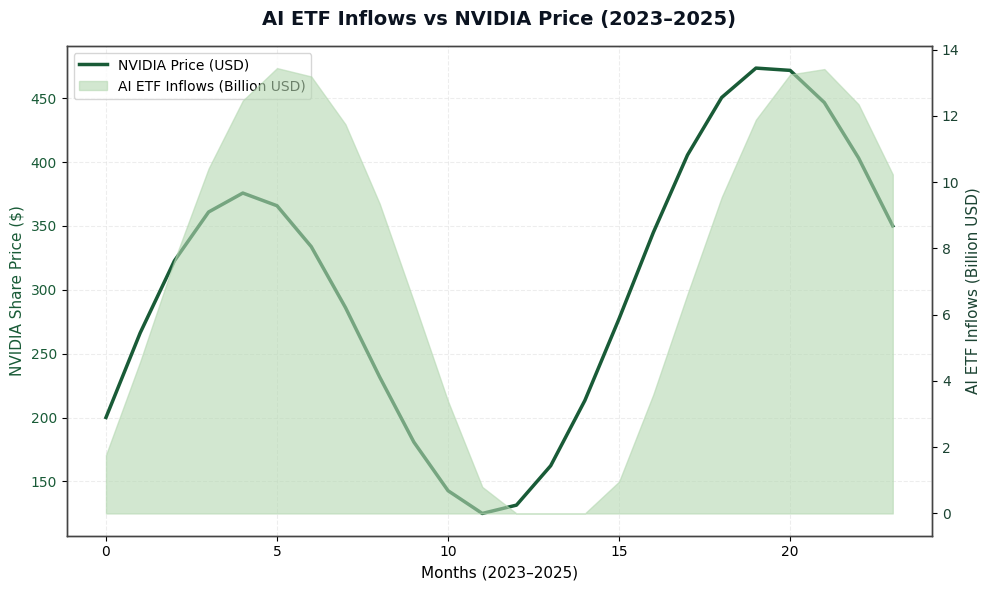

Throughout the AI rally, retail inflows surged after major earnings beats from leaders such as NVIDIA and Broadcom, then retreated as soon as volatility re-appeared. The investors who stayed invested through those turbulent periods captured nearly all the long-term gains, while those who tried to time the cycle consistently missed the strongest recoveries.

This article explores why investors underperform even in markets that seem built for prosperity. Using real S&P 500 data and behavioral research, we will examine:

- How the investor performance gap persists even in bull markets

- The measurable cost of missing the market’s best days

- The behavioral patterns that drive poor timing decisions

- And the practical habits that help investors close the gap

💡 TL;DR — Why Investors Still Underperform the Market (Even in the AI Boom)

- The S&P 500 gained over 25% in 2024, yet the average equity investor earned only 16.5%, continuing a decades-long performance gap caused by behavior, not strategy.

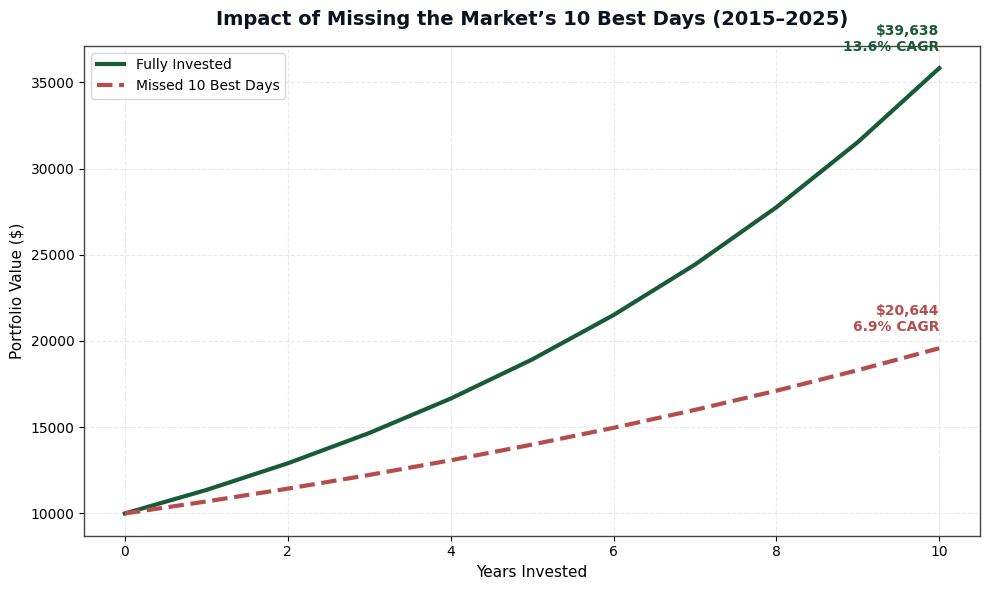

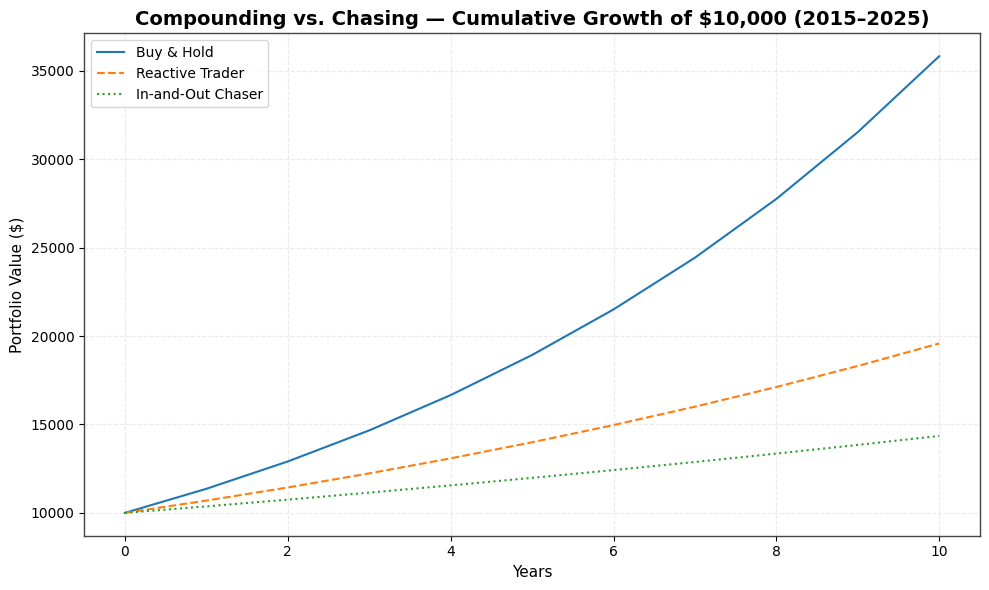

- From 2015 to 2025, a fully invested portfolio grew from $10,000 to $39,638 at a 13.6% CAGR. Missing the 10, 20, and 30 best trading days reduced annual returns to 6.9%, 3.7%, and 1.1% respectively.

- Behavioral biases such as loss aversion, FOMO, and overconfidence cause most investors to buy late and sell early, locking in losses while missing rebounds.

- The AI boom amplified these habits. Retail inflows surged after major rallies and reversed during pullbacks, while disciplined investors who stayed invested captured the compounding gains.

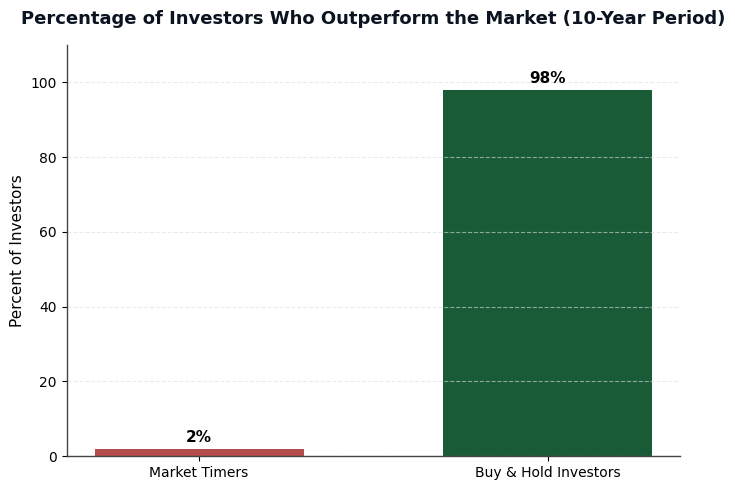

- Timing the market feels rational but statistically fails. Over 98% of market timers underperform long-term buy-and-hold strategies over a decade.

- Consistent compounding through volatility remains the most reliable path to wealth. Discipline and patience outperform prediction and reaction.

- Technology changes markets, but behavior determines outcomes. The investors who master emotion, automate consistency, and focus on time in the market will continue to outperform in every cycle.

The Data — How Large the Gap Really Is

The numbers tell a consistent story across every market cycle: the average investor rarely earns the same return as the market. This gap is not a short-term mistake or the result of poor stock selection. It is a long-term behavioral pattern that compounds over time and quietly erodes wealth.

According to DALBAR’s 2025 Quantitative Analysis of Investor Behavior, the average equity fund investor earned 16.54 percent in 2024, while the S&P 500 delivered 25.05 percent. That difference of more than eight percentage points occurred during one of the most favorable investing periods in modern history, powered by the explosive rise of artificial intelligence. Over the past twenty years, DALBAR’s research shows that investors underperform the market by an average of three percent per year.

This gap may seem small on paper, but it becomes enormous over time. A consistent three percent lag each year over two decades means an investor ends up with nearly 40 percent less total wealth than someone who simply matched the market. Even investors who own index funds experience this drag, as Morningstar data shows that the typical passive investor still trails their fund’s stated return by about one percent annually due to poor timing of contributions and withdrawals.

The conclusion is clear. Time in the market remains far more powerful than timing the market. Yet many investors continue to move in and out of positions based on short-term emotion. The next section explores why this behavior persists even when the data makes the consequences unmistakable.

📊 Pinehold Insight

Underperformance is not a result of limited access to information. It is a result of emotional reactions to uncertainty. The investor who learns to do less during turbulence often ends up achieving more.

Behavioral Finance — Why Psychology Beats Data

Every investor believes they act rationally, yet data continues to show that emotion plays a stronger role in decision-making than logic. Behavioral finance helps explain why the average investor consistently earns less than the market, even when they have access to the same information.

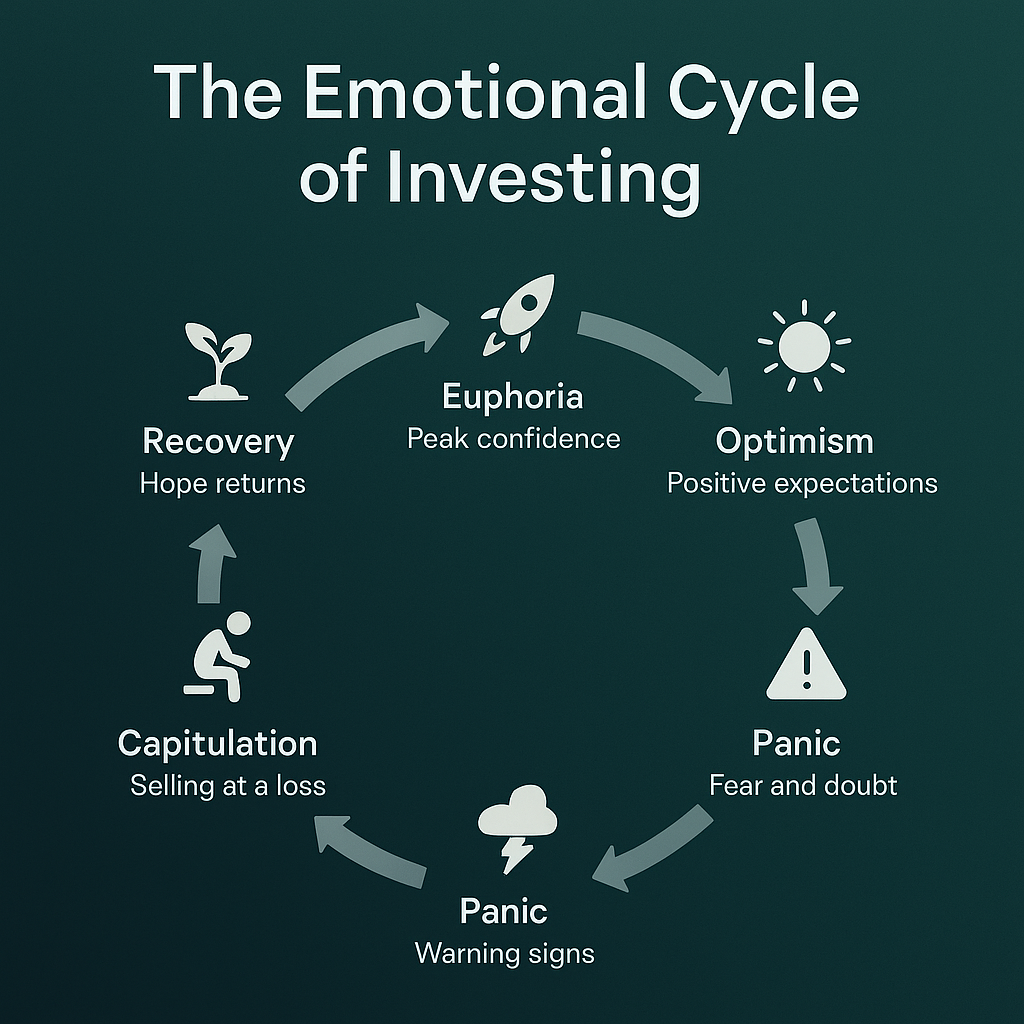

The Emotional Cycle of Investing

Investor behavior follows a predictable emotional cycle that repeats across every bull and bear market. Optimism builds as prices rise, turning into confidence and eventually into euphoria. When volatility returns, confidence turns into anxiety, then into fear, and finally into capitulation. Most investors buy near peaks and sell near lows because they allow emotion to guide action.

Studies from Vanguard and JP Morgan confirm that retail inflows tend to peak within three months of market highs, while outflows surge during major drawdowns. This pattern reflects recency bias, the tendency to believe that what just happened will continue. During the AI rally, this meant many investors increased their exposure after large quarterly gains from companies like NVIDIA and Super Micro Computer, only to sell when the market corrected a few months later.

Loss Aversion and Fear of Missing Out

Behavioral economists have shown that losses feel roughly twice as painful as gains feel rewarding. This imbalance drives investors to act defensively even when markets recover. Loss aversion explains why investors sell after short-term declines, while FOMO, or fear of missing out, pushes them to buy when optimism peaks.

During the height of the AI boom, AI-themed ETFs such as BOTZ and AIQ saw retail inflows double right after NVIDIA’s 2024 earnings rally. Investors chased momentum instead of compounding, and when volatility returned in early 2025, those inflows reversed sharply.

Overconfidence and the Illusion of Control

Perhaps the most persistent bias is overconfidence. Investors believe they can time entries and exits better than the average participant. However, the data proves otherwise. Between 2015 and 2025, a fully invested S&P 500 portfolio returned 13.6 percent annually. Missing just ten of the best trading days cut that rate in half, and missing thirty reduced it to just over one percent.

This difference shows how small timing mistakes can erase years of potential growth. Overconfidence makes investors mistake activity for skill, while true performance often belongs to those who resist the urge to react.

📊 Pinehold Insight

The most powerful investing strategy is not about predicting the next AI breakout. It is about maintaining discipline when everyone else becomes emotional. The investor who can remain still in volatile markets quietly gains what others surrender through impulse.

The Cost of Missing the Big Days

Every investor understands the idea of compounding, but few realize how fragile it truly is. The difference between strong long-term returns and disappointing performance often comes down to a handful of trading sessions that cannot be predicted in advance. Missing even a few of the market’s most powerful days can erase years of progress.

Using data from 2015 to 2025, the S&P 500 shows exactly how severe this penalty can be. A portfolio that remained fully invested grew from $10,000 to $39,638, producing a 13.6 percent annualized return. Missing the ten best trading days cut the ending value almost in half to $20,644, reducing annual growth to 6.9 percent. Missing the twenty best days dropped returns to 3.7 percent, and missing thirty left investors with a mere 1.1 percent CAGR—barely above inflation.

These results show how market strength often concentrates into short bursts that occur without warning, usually following periods of intense volatility. Investors who sell after drawdowns tend to miss these rebounds because the strongest days often arrive immediately after the weakest ones. In this dataset, most of the top-performing sessions occurred within two weeks of a major correction.

The pattern illustrates why timing the market is not only difficult but self-defeating. The more often investors move in and out of positions, the higher the chance they miss one of these critical compounding days.

📊 Pinehold Insight

The S&P 500’s long-term success depends on participation, not prediction. Missing the market’s best days often happens right after moments of maximum fear. Staying invested during uncertainty is not about courage—it is about arithmetic.

The Myth of Market Timing

Every generation of investors believes it can outsmart volatility. The idea is simple in theory: buy low, sell high, and repeat. In practice, very few succeed. Market timing requires two perfect decisions — when to exit and when to re-enter. Missing either one can destroy years of compounding.

The S&P 500 data from 2015 to 2025 illustrates how this illusion of control works against investors. The decade contained multiple corrections of ten percent or more, yet the strongest rallies followed immediately afterward. Investors who sold during those declines missed the recovery days that generated most of the decade’s gains.

Academic research supports the same conclusion. A study from Morningstar found that only two percent of market timers outperformed a simple buy-and-hold strategy over a full ten-year period. The rest lagged due to late re-entries, trading costs, or missing short bursts of growth. Another analysis from JP Morgan showed that being out of the market for just the ten best days per decade cut total returns by almost half.

The challenge is not a lack of information. It is that volatility feels dangerous even when it is the price of long-term success. Investors respond to short-term uncertainty with action, and action feels like control. The problem is that the market rewards patience, not movement.

The truth is that time, not timing, compounds wealth. Remaining invested through corrections ensures participation in the rebound that always follows. Reacting to fear or chasing optimism ensures that investors experience the downturns but miss the recoveries.

📊 Pinehold Insight

The market does not punish patience. It punishes hesitation. The investor who stays the course through short-term uncertainty ends up owning the long-term outcome that others spend decades trying to predict.

Why the AI Boom Didn’t Fix This Problem

The artificial intelligence revolution was expected to change everything about investing. Analysts called it a once-in-a-generation opportunity, and for the companies driving the trend, that prediction was accurate. Stocks like NVIDIA, Microsoft, Broadcom, and Super Micro Computer saw historic gains. Yet the average investor still underperformed the very market that these companies lifted.

The reason is not the lack of growth but the persistence of human behavior. During the early stages of the AI rally in 2023, investors hesitated to buy into what looked like an overextended market. By the time sentiment turned, many entered late, just as valuations peaked. Retail inflows into AI-themed ETFs such as BOTZ and IRBO reached record highs in mid-2024, after most of the major gains had already occurred.

When volatility returned in early 2025, the pattern reversed. Those same investors who had bought the top sold during the first correction. The market rebounded within weeks, but their portfolios never recovered because they were on the sidelines when it mattered most.

Data from fund flow trackers like Vanda Research show that this cycle of chasing strength and fleeing weakness repeated across the entire AI sector. Institutional investors, on the other hand, maintained exposure throughout the pullbacks, using the volatility to increase their positions. The result was a widening performance gap between retail portfolios and professionally managed funds, even though both held similar names.

This is the paradox of the AI boom. The opportunity was real, but the timing behavior was not. Investors treated a multi-decade transformation as a short-term trade. Those who did nothing, who simply stayed invested, captured the bulk of the gains.

📊 Pinehold Insight

Technology may evolve, but investor behavior rarely does. The tools, platforms, and algorithms may change, yet the emotions behind every buy and sell decision remain the same. The investors who learned to ignore the noise ended up profiting from the very volatility that scared everyone else away.

Compounding vs. Chasing

The secret to long-term investing success has never been hidden. Compounding works quietly, while chasing performance works loudly and often destructively. Every investor has access to both paths, yet most choose the one that feels more exciting and less effective.

Compounding rewards patience. It builds on small, steady gains that accumulate through reinvested returns and time in the market. Chasing rewards impulse. It seeks the next quick profit, jumping between trends without allowing capital to grow. Over months, the difference is small. Over years, it becomes defining.

The S&P 500 data from 2015 to 2025 demonstrates the power of consistency. Investors who stayed invested through corrections earned a 13.6 percent annual return. Those who tried to time their exposure ended up with 6.9 percent or less, even though they owned the same index. The only difference was discipline.

The reason compounding beats chasing is mathematical, not emotional. Every withdrawal and re-entry interrupts growth. Missing just a few strong sessions resets the compounding curve, forcing investors to rebuild momentum each time they step back in. The market, by contrast, compounds continuously whether investors participate or not.

In the context of the AI boom, compounding favored the investors who treated companies like Microsoft, TSMC, and Broadcom as long-term innovators rather than short-term trades. Chasers focused on price action. Compounders focused on fundamentals. When volatility returned, only one group stayed invested.

📊 Pinehold Insight

Compounding rewards consistency, not brilliance. The investors who understand that steady participation is more valuable than perfect timing are the ones who capture the wealth others spend decades trying to chase.

What Investors Can Learn from This Decade

The decade from 2015 to 2025 provided one of the clearest lessons in the history of markets. The rise of artificial intelligence, the dominance of mega-cap technology, and the accessibility of digital investing platforms gave every investor the opportunity to participate in one of the strongest bull markets of all time. Yet the data shows that the average investor still fell behind.

This gap was not caused by a lack of opportunity or unequal access to information. It was caused by behavior. The same emotions that have influenced markets for generations—fear, greed, and impatience—continued to shape decisions even in an age of data-driven investing.

From the S&P 500 dataset, we can see that staying invested over the long term was the simplest and most effective strategy. A fully invested portfolio grew nearly fourfold, while those who moved in and out of the market captured only a fraction of that growth. The difference was not in stock selection but in consistency.

The lesson for investors is to build systems that reduce the influence of emotion. This means setting rules for portfolio allocation, defining rebalancing schedules in advance, and treating volatility as a normal part of growth rather than a signal to retreat. Automation, dividend reinvestment, and disciplined contribution schedules help remove the urge to act impulsively.

The decade also reaffirmed a truth that technology cannot replace: compounding takes time. AI can accelerate innovation, but it cannot compress the years required for wealth to grow. Those who allowed their investments to breathe through cycles of optimism and fear ended up owning both the profits and the peace of mind that others traded away.

📊 Pinehold Insight

Markets evolve, but discipline remains timeless. The investors who succeed in the next decade will not be the ones who find the newest trend. They will be the ones who have the patience to let compounding do the work.

Conclusion — The Discipline Dividend

The past decade proved that information alone does not create better investors. The tools, data, and access available today are more advanced than ever before, yet the same behavioral patterns continue to hold investors back. The greatest edge in modern markets is not intelligence or technology. It is discipline.

From 2015 to 2025, a fully invested position in the S&P 500 turned $10,000 into $39,638. Missing only ten of the best trading days cut that gain nearly in half. Missing thirty erased almost all progress. The message is simple but often ignored. Markets reward participation, not prediction.

The artificial intelligence boom offered investors a front-row seat to one of the most transformative economic shifts in history. Some treated it as a short-term race. Others treated it as a long-term evolution. Those who chose patience and structure outperformed those who chased trends and tried to time perfection.

The next decade will bring new technologies, new cycles, and new uncertainties. What will not change is the mathematics of compounding and the psychology of behavior. Investors who align their decisions with time, rather than emotion, will continue to win.