⚠️ Financial Disclaimer

The information provided in this article is for educational and informational purposes only and should not be construed as financial, investment, or trading advice. All data and analysis reflect opinions current as of publication and may change without notice. Always conduct your own research or consult with a licensed financial advisor before making investment decisions. Past performance is not indicative of future results.

As 2025 unfolds, global markets are entering a new phase marked by selective leadership and diverging sector performance. The S&P 500 is up 13.66% year to date, reflecting strong optimism, but the underlying gains are far from evenly distributed.

Investors are watching a market where technology and communication stocks continue to dominate, while several traditional sectors are struggling to keep pace. After two years defined by the artificial intelligence boom and higher interest rates, the landscape now reflects a balance between innovation-driven growth and cautious normalization.

The macro backdrop is shifting as inflation cools, interest rates stabilize, and corporate earnings regain momentum. Productivity growth from AI adoption, automation, and supply chain improvements is beginning to show up in data. At the same time, energy markets, consumer demand, and defensive plays are showing fatigue.

In this environment, understanding which sectors are leading is more important than ever. The rally of 2025 is not broad-based. It is powered by a handful of industries that are capturing both investor capital and fundamental growth. This report breaks down those leaders, the data behind their strength, and what their performance signals for the rest of the year.

💡 TL;DR - Which Sectors Are Leading in 2025

- The market is up 13.66% YTD, but gains are concentrated rather than broad.

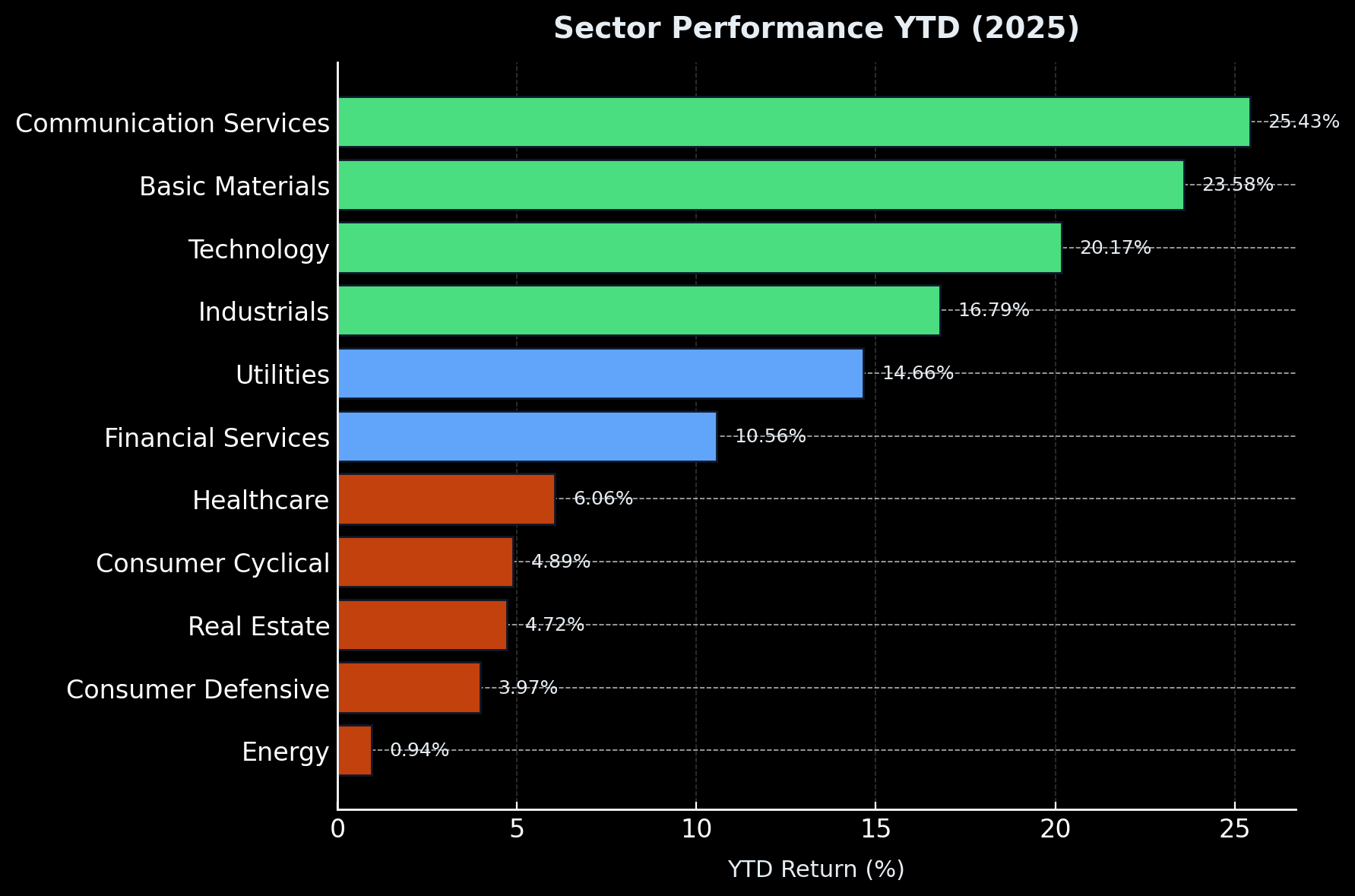

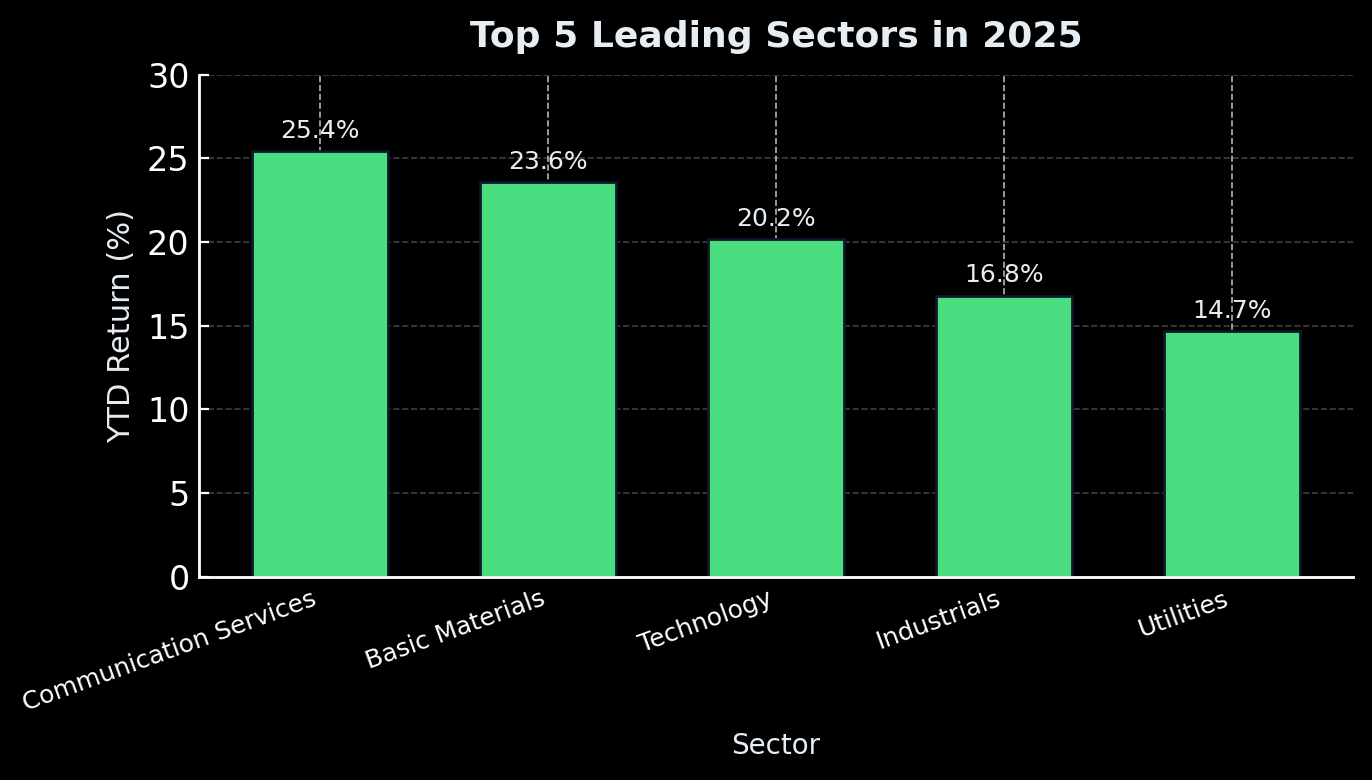

- Top performers: Communication Services +25.43%, Basic Materials +23.58%, Technology +20.17%.

- Technology carries the most influence with a 31.28% market weight, so its moves shape overall returns.

- Industrials and Utilities are solid contributors at +16.79% and +14.66%, helped by infrastructure, electrification, and grid demand.

- Middle ground: Financial Services +10.56% and Healthcare +6.06% provide steady but slower compounding.

- Laggards: Consumer Cyclical +4.89%, Real Estate +4.72%, Consumer Defensive +3.97%, and Energy +0.94%.

- What is driving leadership: AI buildout, stable rates, and fiscal investment favor innovation and real-economy projects.

- Positioning idea: pair AI-focused Tech exposure with Industrials and Materials for balance, while watching for mean reversion in Financials and Healthcare.

Market Overview — Performance at a Glance

The 2025 market is defined by concentration. While the S&P 500 is up 13.66% year to date, most of that performance is driven by a few high-growth sectors. Investors who look beneath the surface see that gains are not evenly spread across the economy.

Below is a snapshot of sector performance based on market-weighted returns across the S&P 500 as of mid-2025.

| Sector | Market Weight | YTD Return (%) |

|---|---|---|

| Technology | 31.28% | 20.17% |

| Communication Services | 10.05% | 25.43% |

| Basic Materials | 2.53% | 23.58% |

| Industrials | 8.52% | 16.79% |

| Utilities | 2.24% | 14.66% |

| Financial Services | 14.69% | 10.56% |

| Healthcare | 8.92% | 6.06% |

| Consumer Cyclical | 10.76% | 4.89% |

| Real Estate | 2.24% | 4.72% |

| Consumer Defensive | 4.91% | 3.97% |

| Energy | 3.87% | 0.94% |

📈 Source: Yahoo Finance

Key takeaway: the average investor holding a market-weighted index is benefiting from strong performance in a few specific areas, not from broad-based strength. Communication Services, Basic Materials, and Technology are responsible for more than half of total market gains.

These results highlight a clear rotation into growth and innovation-oriented sectors, while traditional defensives and cyclical industries have lost momentum. The shift suggests that investors are positioning for continued productivity gains from artificial intelligence and infrastructure spending rather than seeking safety or yield.

The following sections explore how each leading sector is achieving its performance, what is driving their underlying fundamentals, and where opportunities may emerge as the market continues to evolve.

Methodology — What Defines “Leading”

To understand which sectors are truly leading the market in 2025, Pinehold evaluates both quantitative performance and qualitative fundamentals. A sector’s leadership is not determined by price movement alone. Instead, it reflects a combination of sustained earnings strength, capital inflows, and market impact.

1. Total Return

This measures the year-to-date performance, including both price appreciation and dividends. Total return provides the most direct view of investor sentiment and short-term momentum. A strong return signals that investors are willing to pay for exposure to future growth within that sector.

2. Market Weight

Market weight reflects how much influence a sector has on the broader index. A sector that rises sharply but represents a small percentage of total market capitalization may have limited impact on the overall market. Conversely, a large sector like Technology can move the index even with moderate gains.

3. Fundamental Strength

Earnings growth, margin expansion, and forward price-to-earnings ratios help measure whether the current performance is backed by real profit growth. Sustainable leadership typically appears where fundamentals and price action align.

4. Capital Flows and Valuation Trends

ETF inflows, mutual fund allocations, and shifts in institutional ownership show where large pools of capital are moving. These flows can confirm sector leadership or indicate rotation in progress.

Pinehold’s analysis combines these metrics into a sector leadership composite, highlighting which parts of the market are driving returns both by size and by momentum. Using this approach reveals that a handful of high-growth sectors are responsible for most of 2025’s performance, setting the stage for the deeper analysis that follows.

The Clear Leaders of 2025

1. Communication Services (+25.43%) — The Comeback Story

Communication Services is the standout performer of 2025, gaining 25.43% year to date. After lagging the market in 2022 and 2023, the sector has surged back as digital advertising, streaming, and AI-driven media platforms return to growth.

Companies such as Alphabet (GOOGL), Meta Platforms (META), and Netflix (NFLX) have posted strong revenue rebounds as global ad budgets recover. The integration of machine learning into ad targeting and content recommendation systems has increased engagement and improved monetization efficiency.

Subscriber growth in streaming and social media has stabilized, allowing these companies to focus on profitability rather than expansion at all costs. The sector’s resilience reflects both strong cash flows and improved cost discipline.

Although Communication Services represents only 10.05% of the market, it has contributed an outsized share of the S&P 500’s total return this year. Investors are rewarding consistent earnings delivery and scalable digital platforms that continue to benefit from AI integration.

📊 Pinehold Insight

Although Communication Services represents only 10.05% of the market, it has contributed an outsized share of the S&P 500’s total return this year. Investors are rewarding consistent earnings delivery and scalable digital platforms that continue to benefit from AI integration.

2. Basic Materials (+23.58%) — The Sleeper Winner

The Basic Materials sector has quietly emerged as one of the strongest performers of 2025, rising 23.58% year to date. While often overlooked, it has benefited from accelerating demand across multiple industrial and technology-driven value chains.

The surge in AI data centers, electric vehicles, and renewable energy infrastructure has created sustained demand for copper, lithium, aluminum, and rare-earth elements. Supply constraints in key commodities have further strengthened pricing power for producers.

Chemical manufacturers and construction material suppliers are also seeing improving margins as global supply chains normalize and energy input costs stabilize.

📊 Pinehold Insight

Despite its small 2.53% market weight, Basic Materials’ performance signals the early stages of a new industrial investment cycle. The sector’s gains are broad-based and supported by tangible fundamentals, not speculative momentum.

3. Technology (+20.17%) — The Perpetual Engine

Technology remains the cornerstone of the 2025 market, advancing 20.17% year to date. With a 31.28% market weight, it continues to exert the greatest influence on overall market direction.

This year’s growth has come from the AI infrastructure boom. Demand for high-performance chips, advanced networking equipment, and data center power systems continues to outpace supply. Companies such as Nvidia (NVDA), Broadcom (AVGO), Super Micro Computer (SMCI), and Vertiv Holdings (VRT) are capturing the lion’s share of spending in this space.

Software firms are also seeing steady revenue growth as enterprises invest in AI integration, cybersecurity, and cloud automation. The combination of secular tailwinds and expanding productivity has solidified Technology’s role as the market’s structural leader.

📊 Pinehold Insight

Technology’s heavy index weighting means its gains explain nearly one-third of the total market return in 2025. However, elevated valuations increase sensitivity to earnings surprises in the second half of the year.

4. Industrials (+16.79%) — The Reshoring Renaissance

Industrials have advanced 16.79% year to date, reflecting a sustained global investment cycle in manufacturing, logistics, and defense. Fiscal spending from the CHIPS Act, Inflation Reduction Act, and infrastructure programs continues to drive demand for industrial equipment and electrical components.

Companies like Eaton (ETN), Caterpillar (CAT), and Parker Hannifin (PH) have benefited from both private and public capital expenditures aimed at reshoring production capacity. Automation and electrification remain core growth themes.

📊 Pinehold Insight

The Industrial sector’s momentum is underpinned by tangible earnings growth and record backlogs in manufacturing and defense contracts. Investors view it as a balanced way to gain exposure to real-economy growth without relying on speculative multiples.

5. Utilities (+14.66%) — From Defensive to Dynamic

Utilities, long viewed as defensive holdings, have posted a strong 14.66% gain in 2025. The sector is benefiting from a structural increase in electricity demand tied to AI data centers, EV infrastructure, and grid modernization projects.

Companies providing generation capacity, transmission upgrades, and renewable integration have become unexpected beneficiaries of the AI-driven economy. Dividend stability and reliable cash flows continue to attract institutional investors looking for consistent returns with a technological edge.

📊 Pinehold Insight

Utilities now sit at the intersection of traditional stability and modern growth. As power consumption from data infrastructure rises, the sector’s role in supporting AI expansion gives it new relevance for long-term investors.

The Middle Ground — Steady Compounders

Not every sector is surging ahead in 2025, but several are still contributing consistent, moderate gains. These areas may not lead the market, yet they remain essential for balanced portfolios seeking stable earnings and lower volatility.

Financial Services (+10.56%) — Steady Gains in a Normalizing Rate Environment

The Financial Services sector has posted a respectable 10.56% year-to-date return, benefiting from a more predictable interest rate landscape. With the Federal Reserve holding rates steady and inflation continuing to cool, the financial system has regained stability after years of tightening cycles and credit stress.

Major banks are seeing a rebound in lending margins and trading volumes, while asset managers and payment networks are capitalizing on renewed investor activity. The sector’s performance reflects a shift toward fundamentals rather than macro speculation.

📊 Pinehold Insight

Although not a high-growth leader, Financial Services remains a cornerstone of long-term equity exposure. Its performance is tied to capital market health and corporate lending activity, both of which have improved significantly since 2023.

Healthcare (+6.06%) — Reliable but Restricted

Healthcare has risen 6.06% year to date, a modest but steady performance compared to the broader market. The sector remains a defensive anchor, supported by consistent demand, strong cash flows, and global demographic trends.

However, political scrutiny surrounding drug pricing and reimbursement policies continues to weigh on valuations. Biotechnology has also underperformed within the group, offsetting gains in medical equipment and managed care providers.

Pharmaceutical giants have maintained profitability, but investor enthusiasm has cooled relative to higher-growth industries. Healthcare’s strength lies in its stability rather than acceleration.

📊 Pinehold Insight

For investors seeking diversification, Healthcare provides an effective hedge against macro risk. While growth is limited, the sector’s steady earnings profile can buffer portfolios against volatility in technology or cyclicals.

Together, Financial Services and Healthcare form the middle layer of market performance in 2025. They are not driving the rally, but they offer consistent returns supported by durable fundamentals. As valuations in high-growth areas stretch, these sectors may reassert their importance later in the year as capital rotates toward stability.

The Laggards — Rotation Leaves Them Behind

While several high-growth sectors continue to power the market, others have been left behind. These areas are contending with weaker earnings momentum, slowing demand, and reduced investor interest. Their modest returns in 2025 reflect both cyclical challenges and capital rotation toward more dynamic segments of the market.

Consumer Cyclical (+4.89%) — Discretionary Spending Slows

The Consumer Cyclical sector has gained only 4.89% year to date, as household budgets feel the effects of slower wage growth and higher credit costs. Discretionary categories such as apparel, automotive, and consumer electronics have softened after several years of post-pandemic demand.

Retailers are relying heavily on promotions to maintain sales volumes, which is compressing margins across the industry. Although travel and entertainment spending remain relatively strong, investors are showing less enthusiasm for companies tied to short-term consumer confidence.

📊 Pinehold Insight

Consumer Cyclical stocks tend to outperform early in economic expansions, but current market conditions suggest that consumers are becoming more selective. This sector may need a clearer signal of income growth before regaining leadership.

Real Estate (+4.72%) — Stuck Between Rates and Demand

Real Estate has returned 4.72% year to date, lagging the broader market as higher borrowing costs and hybrid work patterns continue to weigh on valuations. Commercial real estate remains under pressure, with office and retail properties struggling to recover occupancy levels.

Residential and industrial REITs have shown modest improvement, supported by housing shortages and e-commerce logistics demand, but the overall sector remains constrained by financing costs.

📊 Pinehold Insight

Real Estate performance is highly sensitive to interest rate expectations. Until yields decline meaningfully, upside will likely remain limited despite long-term structural demand for logistics and housing assets.

Consumer Defensive (+3.97%) — Losing Ground to Growth

Consumer Defensive stocks, which include food, beverage, and household product companies, have gained 3.97% year to date. These firms typically perform well in uncertain environments, but investor attention has shifted toward growth-oriented sectors as economic stability improves.

With inflation moderating, pricing power is fading. Revenue growth has slowed, and valuations now appear elevated relative to the sector’s low single-digit earnings expansion.

📊 Pinehold Insight

Defensive sectors serve as portfolio stabilizers rather than performance drivers. While they may regain relevance during volatility, they currently offer limited upside compared to cyclical and innovation-focused industries.

Energy (+0.94%) — From Leader to Laggard

After dominating performance tables in 2022 and 2023, Energy has posted only a 0.94% gain in 2025. Oil prices have remained range-bound due to balanced global supply and moderate demand growth. Refining margins are under pressure, and exploration budgets have stayed conservative.

Natural gas prices have also softened, while clean-energy firms within the sector are struggling to convert policy support into near-term profits. The result is a sector that is fundamentally stable but no longer driving growth.

📊 Pinehold Insight

Energy’s weak performance reflects normalization rather than decline. After multiple years of outperformance, the sector is now adjusting to slower global expansion and more efficient production capacity.

Taken together, these lagging sectors highlight the market’s narrow breadth in 2025. Investors are focusing capital on innovation and productivity-driven industries while reducing exposure to sectors that depend on consumer strength, interest rate cuts, or cyclical rebounds that have yet to arrive.

Macro Drivers Behind Sector Rotation

The pattern of leadership in 2025 is not random. It reflects a clear alignment between economic fundamentals, policy direction, and investor positioning. The sectors outperforming this year are those directly benefiting from structural trends in technology, productivity, and industrial expansion. At the same time, areas dependent on consumer demand or lower interest rates are under pressure.

1. The AI Adoption Cycle

The single most important macro force shaping market leadership is the ongoing adoption of artificial intelligence across industries. The demand for compute power, semiconductors, and energy infrastructure has created a sustained investment cycle that is driving performance in Technology, Utilities, and Basic Materials.

Capital spending on AI data centers, chips, and cloud services is now one of the largest contributors to global fixed investment growth. This dynamic has shifted investor focus away from short-term consumption and toward long-term infrastructure and innovation.

2. Stabilizing Interest Rates

After several years of monetary tightening, interest rates have stabilized, creating a more predictable environment for corporate planning and capital allocation. This stability benefits Financial Services, Industrials, and Utilities, all of which rely on steady borrowing costs and consistent economic growth.

The absence of rate volatility has reduced uncertainty for both lenders and borrowers, allowing credit conditions to improve. Sectors that struggled under high-rate regimes, such as real estate and consumer discretionary, are still recovering but remain sensitive to further policy shifts.

3. Fiscal Investment and Industrial Policy

Fiscal spending continues to play a key role in supporting industrial activity. Government initiatives under the Infrastructure Investment and Jobs Act, the CHIPS Act, and the Inflation Reduction Act are still in motion. These programs have provided long-term visibility for firms involved in construction, materials, and manufacturing.

The result is a steady pipeline of capital expenditures across domestic production and energy transition projects. This environment supports Industrials and Materials while encouraging corporate investment in productivity-enhancing technologies.

4. Commodity and Supply Chain Normalization

Global supply chains have largely stabilized after years of disruption, creating more predictable input costs for producers. Commodity prices are no longer experiencing the sharp swings of the previous cycle, allowing sectors like Materials, Industrials, and Technology to manage costs effectively.

At the same time, the normalization of energy markets has constrained Energy sector gains, as efficiency and balanced supply offset earlier price volatility.

5. Investor Rotation Toward Secular Growth

The final driver of 2025’s leadership pattern is the continued rotation toward long-term growth themes. Institutional investors are prioritizing exposure to sectors with structural tailwinds such as AI infrastructure, electrification, automation, and cloud computing.

This capital shift has strengthened leadership in Technology, Communication Services, and Utilities, while leaving cyclical and defensive groups behind. It reflects an environment where investors prefer innovation over income and scalability over stability.

In combination, these factors have produced a market where leadership is concentrated but rational. The sectors outperforming in 2025 are supported by real capital investment and measurable productivity gains, suggesting that the rotation is more durable than speculative.

Forward Outlook — H2 2025 and Beyond

The second half of 2025 presents a more nuanced landscape for investors. While the year’s early performance has been dominated by technology and communication stocks, leadership is beginning to show signs of broadening. Several indicators suggest that the next phase of the market may favor sectors with more balanced valuations and exposure to real-economy growth.

1. Mean Reversion Potential

Sectors such as Energy, Healthcare, and Financial Services are showing the early signs of stabilization after periods of relative underperformance. If market breadth continues to improve, these groups could capture incremental flows as investors rotate out of overextended positions in technology and communication.

Healthcare’s earnings reliability and Financials’ improved credit outlook make them logical beneficiaries of any pullback in high-growth valuations. Energy could also recover modestly if global demand strengthens in the winter months or if OPEC production adjustments support pricing.

2. Continued Strength in Industrials and Materials

The tailwinds driving Industrials and Basic Materials remain intact. Infrastructure investment, defense spending, and reshoring trends continue to provide multi-year visibility for manufacturers and suppliers.

Capital expenditures on energy grids, semiconductors, and construction are likely to sustain demand through 2026. These sectors may not match the explosive gains of early 2025, but their underlying growth appears durable and supported by fiscal policy.

3. Technology and Communication: High Quality but Fully Priced

Technology and Communication Services remain the most profitable sectors in the market, but valuations now reflect high expectations. Earnings delivery will be critical through the second half of the year.

Investors are increasingly differentiating between early-stage AI infrastructure providers with tangible growth and software platforms with slower scalability. Any earnings miss or delay in AI monetization could trigger short-term volatility, though the long-term trend remains constructive.

4. ETF and Capital Flow Trends

ETF data for 2025 shows increasing inflows into XLB (Materials) and XLI (Industrials), outpacing XLK (Technology) for the first time since 2023. Institutional positioning is gradually broadening as investors seek exposure to sectors with lower correlation and better value-to-growth ratios.

This reallocation does not suggest a rotation away from innovation but rather a diversification of capital toward infrastructure and tangible growth assets.

5. Election Year Volatility

With the U.S. presidential election approaching, short-term volatility is likely to rise. Fiscal policy expectations, tax discussions, and regulatory themes may temporarily influence sector performance. Historically, election years bring increased trading volume and defensive positioning in late summer, followed by renewed risk appetite once uncertainty clears.

Investors should expect choppier conditions in the third quarter, particularly for sectors sensitive to regulation such as Healthcare, Energy, and Technology.

Pinehold Outlook Summary

Pinehold’s base case projects continued strength in Technology, Communication Services, and Industrials, with gradual improvement in Financials and Healthcare as the year progresses. The emphasis for investors should be on balancing innovation exposure with real-economy participation.

Markets are shifting from a narrow leadership structure to a more rotational phase. This broadening of participation could set the stage for more sustainable growth heading into 2026.

Conclusion — The Shape of Leadership in 2025

The 2025 market tells a clear story of selective strength. Gains are concentrated in the sectors that represent the backbone of the modern economy: Technology, Communication Services, Industrials, and Basic Materials. Each reflects a different aspect of the same transformation taking place across global markets. Artificial intelligence, digital infrastructure, reshoring, and materials demand are creating a new foundation for productivity and growth.

This year’s performance confirms that investors are rewarding sectors supported by both innovation and tangible output. Technology remains the engine, Communication Services captures the monetization of data, Industrials build the infrastructure to sustain it, and Materials supply the inputs that make it possible.

At the same time, lagging areas such as Energy, Consumer Cyclical, and Real Estate are not broken; they are adjusting to a slower cycle. These sectors may become more attractive if valuations compress further or if policy shifts introduce fresh demand catalysts. Market leadership always evolves, and the next rotation will likely begin from the current underperformers.

For investors, the key takeaway is balance. Exposure to AI-driven innovation remains essential, but combining it with positions in industrial and material assets provides resilience if the growth trade cools. The market is no longer reacting to headlines—it is rewarding sectors that produce real earnings and measurable productivity.

As 2025 moves into its final quarters, leadership is not just about performance. It is about durability, fundamentals, and adaptability. The sectors leading today are those redefining how the global economy operates tomorrow.