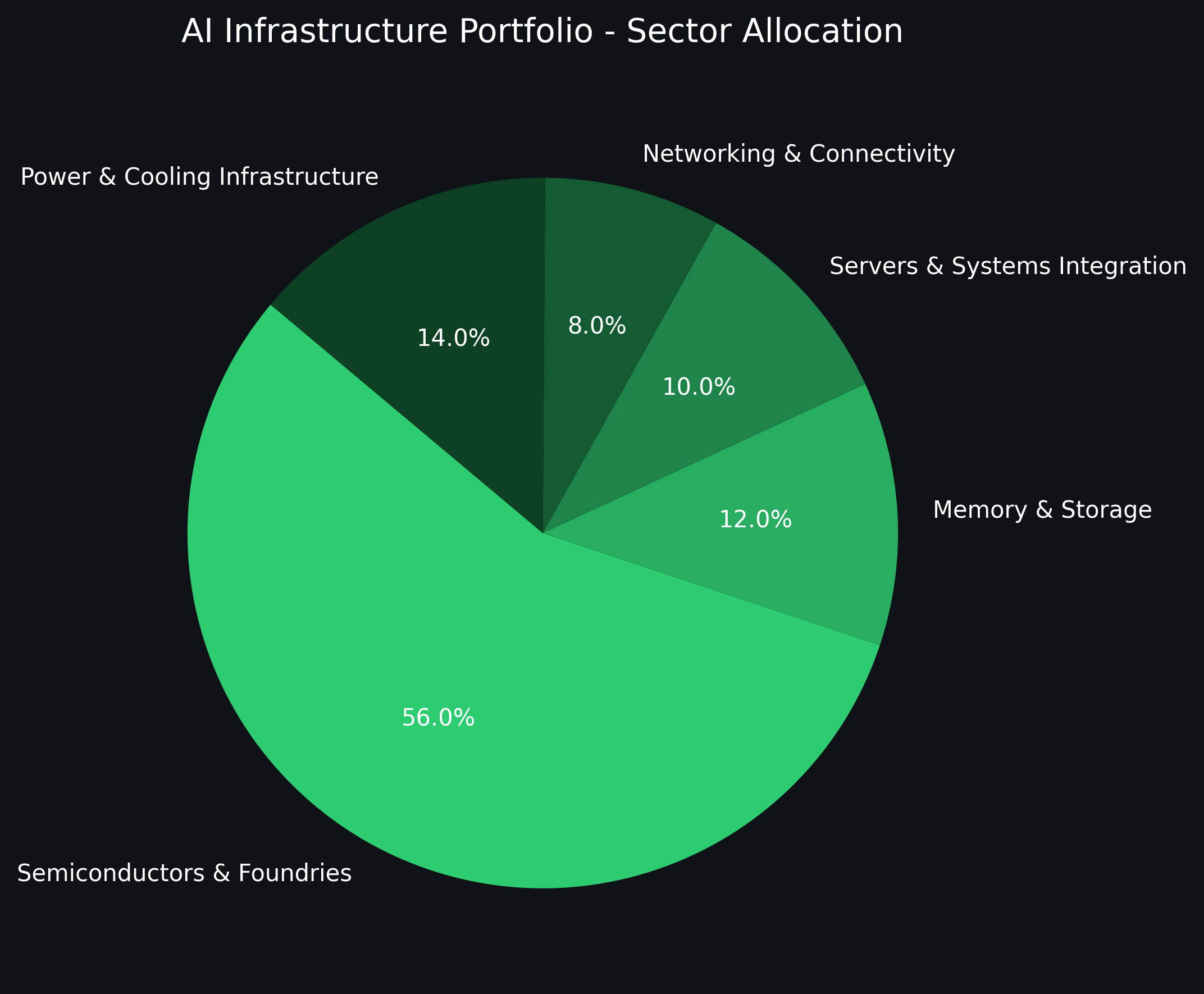

Sector Allocation

The AI Infrastructure Portfolio is diversified across the critical layers of the artificial intelligence supply chain, from semiconductor fabrication and memory to networking, servers, and power infrastructure. Each sector plays a distinct role in enabling the compute capacity and efficiency required for AI expansion.

| Sector | Holdings | Representative Companies | Portfolio Weight | Role in AI Ecosystem |

|---|---|---|---|---|

| Semiconductors & Foundries | 4 | NVIDIA (NVDA), Broadcom (AVGO), TSMC (TSM), ASML (ASML) | 56% | The computational and manufacturing backbone of AI. These companies design, fabricate, and equip the chips powering AI models and data centers. |

| Memory & Storage | 1 | Micron (MU) | 12% | Supplies high-bandwidth memory (HBM) and DRAM critical for training and running large AI models. |

| Servers & Systems Integration | 1 | Super Micro Computer (SMCI) | 10% | Delivers GPU-optimized servers and rack-scale systems that convert chip performance into usable compute power. |

| Networking & Connectivity | 1 | Arista Networks (ANET) | 8% | Enables ultra-fast data transfer between GPUs and across clusters through 400G–800G networking systems. |

| Power & Cooling Infrastructure | 2 | Vertiv (VRT), Eaton (ETN) | 14% | Provides the physical foundation of AI data centers — managing power delivery, grid connections, and advanced thermal systems. |

Summary:

The portfolio maintains a semiconductor-heavy weighting (56%), reflecting the core importance of compute, fabrication, and chip supply in AI growth. Supporting allocations to memory, infrastructure, and networking provide diversification across the full AI value chain balancing high-growth technology exposure with steady infrastructure-driven performance.

Updated on Oct 17, 2025